China EV Market Hits 62.92% Penetration in June 2026 as Gasoline Car Sales Collapse 39%

July 14th, 2026

By EVCUBE .NET

No Comments

In June 2026, more than three out of every five new cars sold in China were either battery electric or plug-in hybrid. The numbers tell a dramatic story: NEV penetration hit 62.92% for the third consecutive record-setting month, while gasoline-only vehicle sales plunged 39% year-over-year. China’s auto market is undergoing a transformation so rapid and so decisive that it is reshaping global automotive strategies in real time.

The latest data, released in early July 2026 by the China Passenger Car Association (CPCA), paints a picture of an industry at a tipping point. Overall automobile sales in China fell 23.2% compared to June 2025, continuing a decline that has been accelerating since March. But within that headline decline lies a tale of two markets: one that is thriving and one that is collapsing.

The Numbers That Matter

New energy vehicle sales in China, which include battery electric vehicles (BEVs) and plug-in hybrid vehicles (PHEVs), reached 1.008 million units in June 2026. That is a 9.4% decline compared to June 2025, marking a surprising dip. But context is everything: the overall passenger car market contracted far more sharply, meaning NEVs actually gained substantial market share.

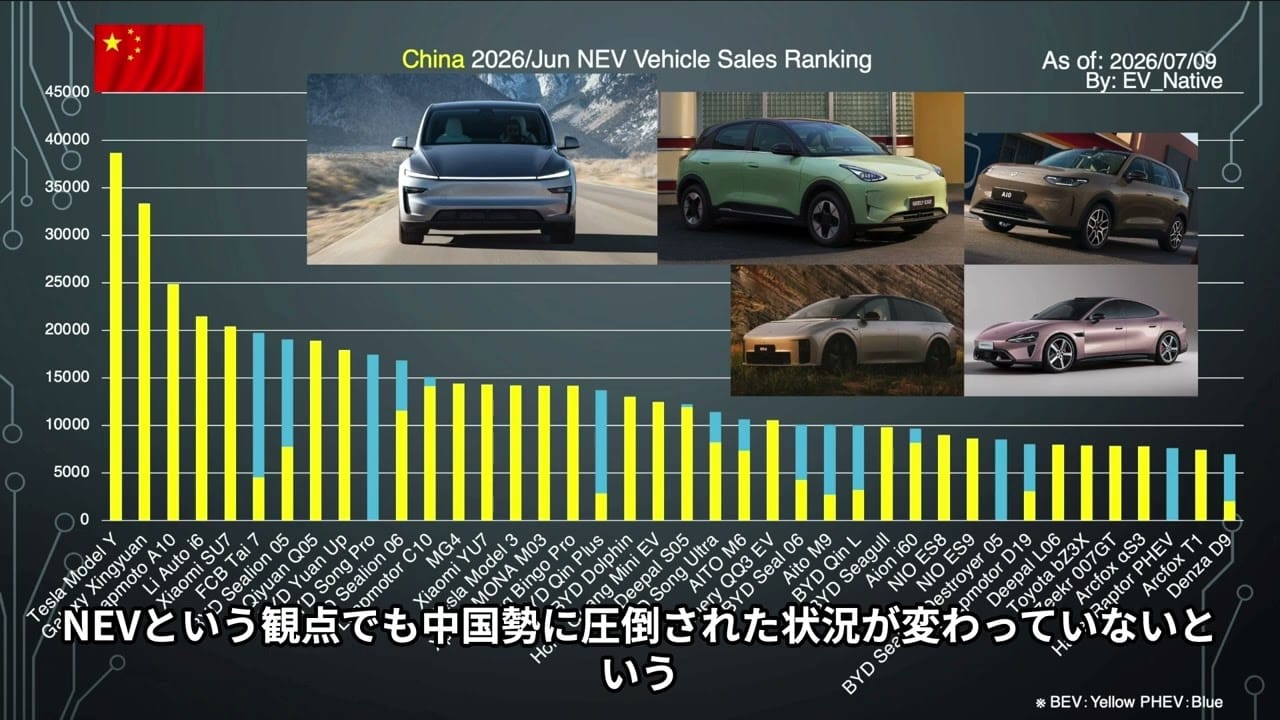

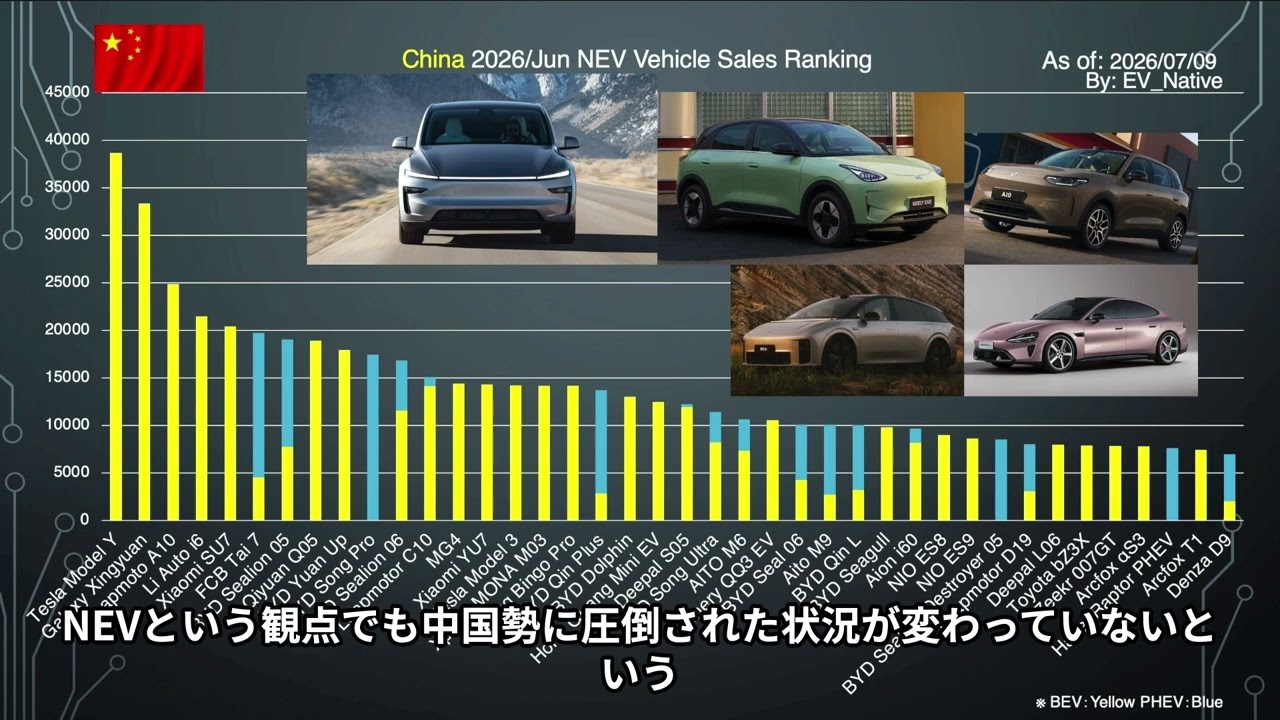

62.92% NEV penetration rate in China, June 2026 ? a new all-time record for the third consecutive month

+42% Battery EV sales growth YoY, significantly outpacing the broader market

-39% Gasoline-only vehicle sales decline in June 2026 ? the sharpest drop on record

Battery electric vehicles performed particularly well, achieving growth of over 42% year-over-year. This is the real engine of the transition. PHEVs and extended-range EVs (EREVs), while still popular, are beginning to face headwinds. Starting in 2027, China will fully eliminate the vehicle purchase tax exemption for PHEVs and EREVs, putting them on equal footing with gasoline cars for the first time. That policy shift is already influencing manufacturer strategies and consumer choices.

China’s NEV penetration rate has set new records for three consecutive months, reaching 62.92% in June 2026. Source: CPCA data via EV Immortal

A Tale of Two Markets

To understand what is happening in China, it helps to look at the market in segments. The mass-market segment, roughly equivalent to vehicles priced between 100,000 and 200,000 RMB ($14,000 to $28,000 USD), is where the fiercest competition is unfolding. BYD continues to dominate this space with its Dynasty and Ocean series, but new entrants are making aggressive moves.

Xiaomi, the smartphone giant turned automaker, has emerged as one of the most watched players. Its SU7 sedan has exceeded expectations, and the company is preparing to launch a larger model ? internally referred to as the “Skyline” project ? in late August. Industry analysts believe this vehicle could reshape the premium EV segment in the same way Xiaomi disrupted the smartphone market: by offering high specifications at aggressive prices.

Segment

Key Players

NEV Share (Est.)

Trend

Budget (under 100K RMB)

BYD Seagull, Wuling Mini EV

~85%

Stable growth

Mass Market (100K-200K RMB)

BYD, Geely, XPeng, Xiaomi

~65%

Intensifying competition

Premium (200K-350K RMB)

NIO, Li Auto, Tesla, Zeekr

~55%

Consolidation underway

Luxury (350K+ RMB)

NIO, Mercedes-EQ, BMW i

~35%

Slowest transition

The Gasoline Car Massacre

The most striking statistic from the June report is not about EVs at all. It is about what they are replacing. Gasoline-only vehicle sales fell 39% year-over-year. That is not a decline; that is a collapse. And it has been building since March.

Joint venture brands that once dominated China ? Volkswagen, Toyota, Honda, Nissan ? are bearing the brunt of this shift. These manufacturers built their Chinese businesses on gasoline-powered sedans and SUVs. As Chinese consumers abandon internal combustion at an accelerating rate, these companies face an existential challenge in what was once their most profitable market.

Honda, in particular, is in a precarious position. The company has confirmed it will not introduce any new electric vehicles in China during 2026. That means facing the remainder of the year with an aging lineup of primarily gasoline models in a market where more than 60% of new buyers are choosing electric. Nissan, to its credit, has acknowledged the problem publicly. Toyota continues to insist its “wait and see” strategy is working, even as its global sales have declined for six consecutive months.

The competitive dynamics in China’s EV market are increasingly favoring domestic manufacturers over joint venture incumbents.

What This Means for the Global Auto Industry

China accounts for roughly 60% of global EV sales. When China sneezes, the global auto industry catches a cold. Several implications are worth watching:

1. The export wave is only beginning. Chinese automakers exported over 5 million vehicles in 2025, and that number is on track to grow significantly in 2026. With domestic production capacity far exceeding domestic demand, Chinese brands are aggressively targeting markets in Southeast Asia, Europe, Latin America, and the Middle East.

2. Price compression is accelerating globally. The intense competition in China’s mass market segment has driven EV prices down dramatically. A BYD Seagull now starts at under 70,000 RMB (approximately $9,700 USD) in China. When Chinese manufacturers scale exports, these price advantages will pressure incumbent automakers in every market.

3. The PHEV bridge is expiring. China’s decision to end tax exemptions for PHEVs and EREVs from 2027 signals that policymakers view the transitional technology as having served its purpose. This will accelerate the shift toward pure battery electric vehicles in the world’s largest auto market.

4. Joint ventures face a reckoning. The business model that sustained Volkswagen, GM, Toyota, and Honda in China for decades ? 50:50 joint ventures producing gasoline cars ? is dying. Those that cannot pivot fast enough to competitive EV lineups will face irreversible market share losses.

Key Market Signals for H2 2026

NEV Penetration63%

Battery EV Growth+42%

Gasoline Decline-39%

Total Auto Market-23.2%

Looking Ahead: H2 2026 and Beyond

The second half of 2026 promises to be even more eventful. Several key developments are on the horizon:

Xiaomi’s larger EV, code-named “Skyline,” is expected to launch in late August. Given Xiaomi’s track record of disrupting established markets, this launch could significantly alter competitive dynamics in the premium segment. Manufacturers that have not yet established a strong EV brand presence may find themselves squeezed out.

The end of PHEV tax exemptions in 2027 will begin to influence purchasing decisions in the second half of 2026, as consumers factor the coming price increase into their buying calculations. This could create a near-term boost for PHEV sales as buyers rush to beat the deadline, followed by a structural shift toward BEVs.

Perhaps most significantly, the question is no longer whether China’s auto market will go fully electric, but how fast. At the current trajectory, NEV penetration could reach 70% by the end of 2026. For global automakers, the message is unambiguous: adapt to China’s electric reality or risk becoming irrelevant in the world’s largest car market.

Is China’s EV market really 62.92% electric?

Yes, based on CPCA data for June 2026. This includes both battery electric vehicles (BEVs) and plug-in hybrid vehicles (PHEVs). The pure BEV share alone grew over 42% year-over-year. The 62.92% figure reflects the combined NEV category, which is the standard metric used in Chinese auto industry reporting.

Why did overall NEV sales decline 9.4% while market share increased?

The total passenger car market contracted sharply ? down 23.2% year-over-year ? due to broader economic factors. Within that shrinking market, NEVs held up much better than gasoline cars, which fell 39%. So while NEV unit sales dipped slightly, their share of the total market rose to a record 62.92%. This is a classic example of relative outperformance in a down market.

Sources & Further Reading

China Passenger Car Association (CPCA) ? June 2026 sales data

EV Immortal ? “Gasoline Car Sales Are Plummeting / First Half of 2026: Report on EV Sales Trends in China” (July 10, 2026)

IEA Global EV Outlook 2026

China Ministry of Industry and Information Technology ? NEV tax policy announcements

Discover the most attractive leasing and financing options for electric vehicles (EVs) this November 2024. Whether you’re looking to lease or finance, there are some excellent deals available that cater…

Walmart’s EV charging network added 12 new stations and 100 stalls in June 2026, now reaching 73 locations and 612 stalls across the US. With California stores now appearing on…

Q2 2026 US EV sales data is in, and this is the weirdest quarter yet. Some brands are down 60% while others just posted their best quarter in history. After…

Stellantis has launched the adorable Fiat Topolino electric quadricycle in the US starting at $13,995 — making it America’s cheapest new car. But there’s a catch: it’s limited to 19…

Chinese EV brands are leading the global charge. ABC News’ analysis reveals how companies like BYD, CATL, and NIO transformed from domestic players into global powerhouses that now dominate the…

California has approved a groundbreaking program offering up to $20,300 in incentives for rideshare drivers to switch to electric vehicles. The program targets low- and moderate-income drivers who complete high…